After publishing the post on whether to take CPP early or late, a friend pointed out to me that if the situation was that the person retired earlier than the example, the conclusion may change. It occurs when the person has less than 40 years of contributions to CPP which can occur if you retire before 58, are unemployed for some years, or work outside Canada for part of your career. In the previous post the example person retired at 60 and had 40 years of CPP contributions.

Just a note on terminology. When I say retire, I mean when the employment stops and stop CPP contributions. This is not the same as the age they start CPP benefits.

When calculating your CPP benefit, the benefit is based on your average (inflation adjusted) pensionable earnings (on which your contributions are made) over your working life. If you earned more than the maximum pensionable earnings in a year the value is capped at that maximum, which is about $55k now. In the calculation you get to drop your 17% of lowest earning years, or in other words keep 83% of your highest pensionable earning years.

Say you stopped working or retired early at 50 and had 28 years of pensionable earnings (YPE) that were at least as high as the maximum pensionable earnings. If you take CPP at 65, you count the average YPE for 39 years ( 39=(65-18)*0.83 ) which will include 11 years of 0. If you take CPP at 60 you count the average YPE for 35 years ( 35=(60-18)*0.83 ) which only includes 7 years of 0 and this average will be higher. The actuarial adjustment of 0.6% per month for taking CPP early will still make the amount starting at 60 lower than starting at 65, but not as low as the actuarial adjustment alone.

I have a CPP Calculator spreadsheet that I used to do the example below. You can find that spreadsheet here.

Lets look at an example.

Consider a person who is currently age 60, retired at 50 and had worked for 28 years from 1978 to 2005. In each of those 28 years they earned at least as much as the CPP maximum pensionable earnings (which was $41,100 in 2005). The inputs and results from the CPP Calculation spreadsheet are shown below.

If they start CPP at age 65, they will receive $10,331 per year starting in 2021, which when adjusted for inflation (CPI) is $9,357 in todays dollars. If we change the CPP start to 60, the amount they will receive (in todays dollars) is $6744. The Actuarial Adjustment for starting CPP at 60 is 64%, so you would have expected to receive $5988 (0.64 * 9357), but due to the effect we discussed above, they receive about $800 more.

Below is a table of values for starting CPP between 60 and 70 for this example. All the values are in todays money (for 2016). The "after Actuarial Adjustment" is the value the person will receive as calculated in the spreadsheet. The "Ratio of ..." column is the ratio of the benefit amount divided by the benefit amount for starting at 65. Normally this would be just the Actuarial Adjustment, but in this special case it is different. Taking CPP starting at 60 in this case the person receives 72% of the benefit relative to starting at 65, not the 64% as per the Actuarial Adjustment.

| CPP | Before | After | Ratio of | |||

| Start | Actuarial | Actuarial | Actuarial | Benefit to | ||

| Age | Adjustment | Adjustment | Adjustment | Start at 65 | ||

| 60 | 10538 | 6744 | 64.0% | 72.1% | ||

| 61 | 10290 | 7326 | 71.2% | 78.3% | ||

| 62 | 10054 | 7882 | 78.4% | 84.2% | ||

| 63 | 9815 | 8402 | 85.6% | 89.8% | ||

| 64 | 9584 | 8894 | 92.8% | 95.1% | ||

| 65 | 9357 | 9357 | 100.0% | 100.0% | ||

| 66 | 9357 | 10143 | 108.4% | 108.4% | ||

| 67 | 9357 | 10929 | 116.8% | 116.8% | ||

| 68 | 9357 | 11715 | 125.2% | 125.2% | ||

| 69 | 9357 | 12501 | 133.6% | 133.6% | ||

| 70 | 9357 | 13287 | 142.0% | 142.0% | ||

Because the benefit does not drop as much in this case then it may be worth for this person to take CPP earlier than the person in my example in the previous CPP blog post.

I have the benefit values for all CPP start years for this example, so I just repeat the calculation using the Retirement Forecaster spreadsheet to find the optimum year to start CPP for a range of life expectancy.

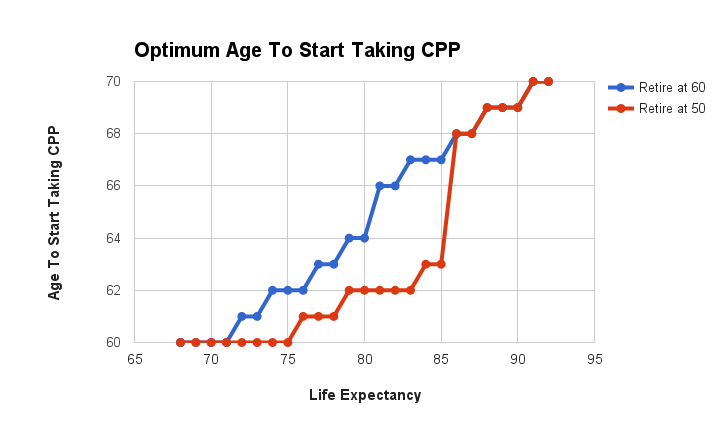

The chart below shows the results from the previous blog post for the person who retired at 60 (blue line) and the results for this new person who retired at 50 (red line). You can see that the conclusion is to take CPP much earlier, if life expectancy is less than 86.

However, this calculation is only to find the optimum, which I defined as the CPP start age that gave the highest Estate value for the person for a specific life expectancy. Lets take a look at how much difference it makes in actual $ amounts. Consider a life expectancy of 84. You can see from the chart above that the optimum for the "Retire at 60" case was 67 and for the "Retire at 50" case is changed by 4 years to 63. The highest estate value is $388,600 for starting CPP at 63. The value for starting CPP at 67, which was the recommendation from the blue line above, is $387,900 which is only $700 less than the optimum. In fact the estate values vary very little in the table below, which makes the value to the person very insensitive to which age they start CPP.

| CPP | Estate Value | ||

| start age | (Current $k) | ||

| 60 | 383.2 | ||

| 61 | 386.5 | ||

| 62 | 388.3 | ||

| 63 | 388.6 | ||

| 64 | 387.7 | ||

| 65 | 385.6 | ||

| 66 | 387.3 | ||

| 67 | 387.9 | ||

| 68 | 387.4 | ||

| 69 | 385.9 | ||

| 70 | 383.2 | ||

Conclusion

This example where the person has less than 40 years of contributions to CPP, does change the optimum age at which to start CPP (relative to a person with 40 or more years of contributions). However the person is only forgoing a very small value if they had used the recommendation in the previous blog post (for those with greater than 40 years of contributions).

If your personal situation is like the example in this blog post or my previous post, you may be able to use the charts to determine when to start taking CPP. If your situation is quite different, then you should do the calculation for yourself. You can determine your CPP benefit using my CPP Calculator spreadsheet, or use the Service Canada calculator. You can put those values in the Retirement Forecaster spreadsheet to determine the optimum for yourself.

Disclaimer: These posts are not fully comprehensive financial advice. You should seek your own qualified investment, tax and legal advice.

No comments:

Post a Comment